17 September, 2020

Australia has officially entered recession for the first time in nearly 30 years, and with the continued presence of COVID-19, we may be in for a protracted period of economic fallout.

Australia has officially entered recession for the first time in nearly 30 years, and with the continued presence of COVID-19, we may be in for a protracted period of economic fallout.

At Raiz, we’re committed to helping our customers take control of their finances by making money management as easy, affordable, and intuitive as possible.

That’s why Raiz has partnered with bundll to create the new Raiz x bundll digital Mastercard for our customers. It provides flexibility, convenience, and budgeting power over how and when you pay for purchases.

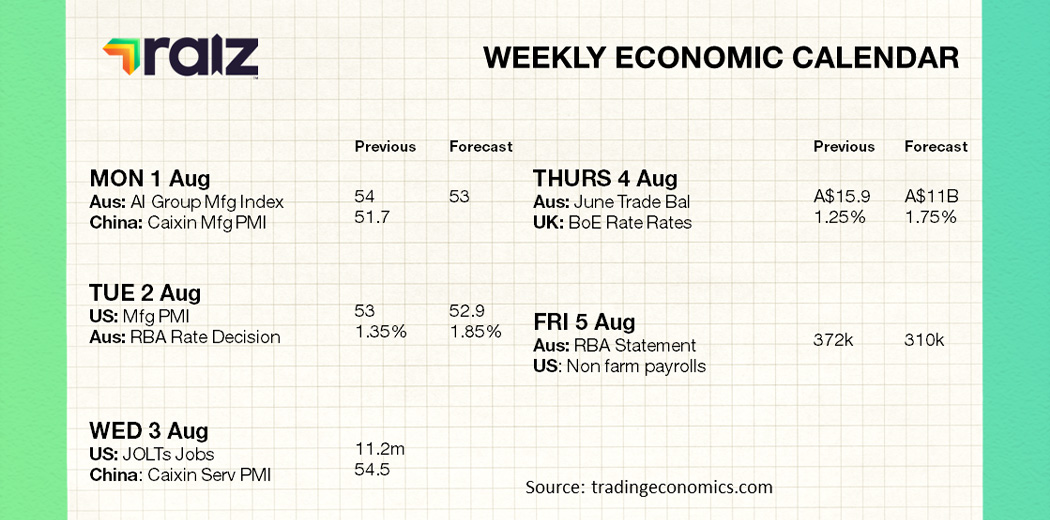

Want to get some context on these upcoming global economic data points and understand what they mean? Raiz has you covered! Read Post

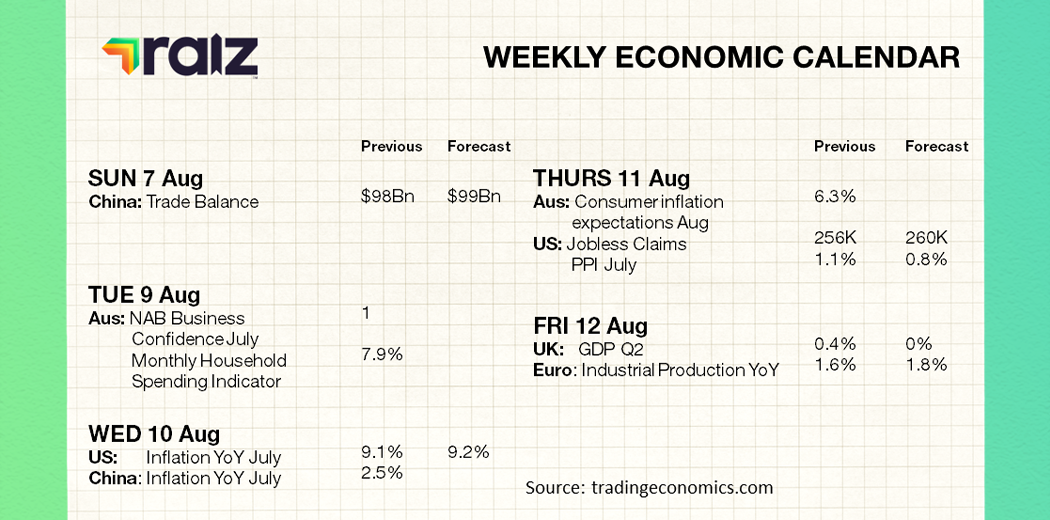

Want to get some context on next week’s global economic data points and to understand what they mean? Raiz has you covered! Read Post

You’re probably thinking that this question is too dependent on a multitude of different factors to give a definitive answer. We agree, but nonetheless thought it’d be an interesting proposition to explore. After analysing some data and applying a few assumptions, we came up with some interesting results.

We can source this information from research by the Australian Automobile Association (AAA). Every quarter they release a report that calculates the average weekly transport cost for the typical Australian household. The report goes into some detail, breaking down costs by state, capital cities and regional areas.

To calculate average costs, the report takes what it considers a typical household, and then applies transport-related expenses (up-font and ongoing) to the hypothetical household based on its lifestyle and family composition. The characteristics of the household reflect the most common characteristics of the Australian population.

The hypothetical city household characteristics:

For the purpose of this post, we’ll look at the transport costs for a typical household in Sydney.

| Expense | Cost a week |

| Car loan repayments | $132.51 |

| Registration and licensing | $26.6 |

| Insurance | $24.76 |

| Servicing and tyres | $29.8 |

| Fuel | $75.05 |

| Public Transport | $50 |

| Tolls | $83.68 |

| Roadside Assist | $2.12 |

| Total | $424.52 |

* Does not consider costs of vehicle depreciation or parking.

For the average Sydney household, transport costs $424.52 a week or $22,075 a year. Knowing this, let’s see if we can calculate the cost of transport for this household if we substitute the expense of owning and operating their cars for the exclusive use of Uber.

Most people will agree that seeing the approximate fare for an Uber, before ordering it, is one of the apps best features. But how is this calculated? Well, this information is available on their website and is calculated as follows:

| Component | Cost |

| Base Fare | $2.50 |

| Booking Fee | $0.55 |

| Per-minute | $0.40 |

| Per KM | $1.45 |

If you’re riding in NSW, a levy of $1.10 is also charged for each trip.

Our data shows that the average Uber fare for a Raiz user is $22.78. An interesting fact, but not very useful in determining the cost for a typical household to replace their cars with Uber.

What we can do is use the typical households distance travelled, as outlined by the AAA report, and plug these numbers into the Uber fare formula.

Let’s assume that a family lives 20 kilometres from the CBD, and that during peak hour, it takes about 45 minutes to get to and from their workplace in the CBD. The cost per commute would be about $59.52 (before tolls). Assuming they work five days a week it would cost $595.2 a week to Uber to work.

We can see that, for the typical household, the cost of just one parent to replace their commute to work with Uber rides has already surpassed the weekly costs of a car. Once you factor in all their regular driving outside of work, it gets much more expensive. We can make some very rough guesses on how much this would be.

According to a the latest AAA road congestion report, the average travelling speed on Sydney roads is 59.6 km/h. As outlined, the typical household travels a total of 25,000 kilometres a year. If they are travelling at the average Sydney speed, this would equate to a travel time of 419 hours or about 25,000 minutes.

Using these numbers, Uber is going to cost $889 a week, even before factoring in base fares, booking fees, tolls, and the NSW levy.

If we assume that each Uber trip is 15 kilometres, the household would be doing 1666 trips a year. That brings the total cost to $1022.38 a week (before tolls), more than double the cost of a typical family that drives their own cars.

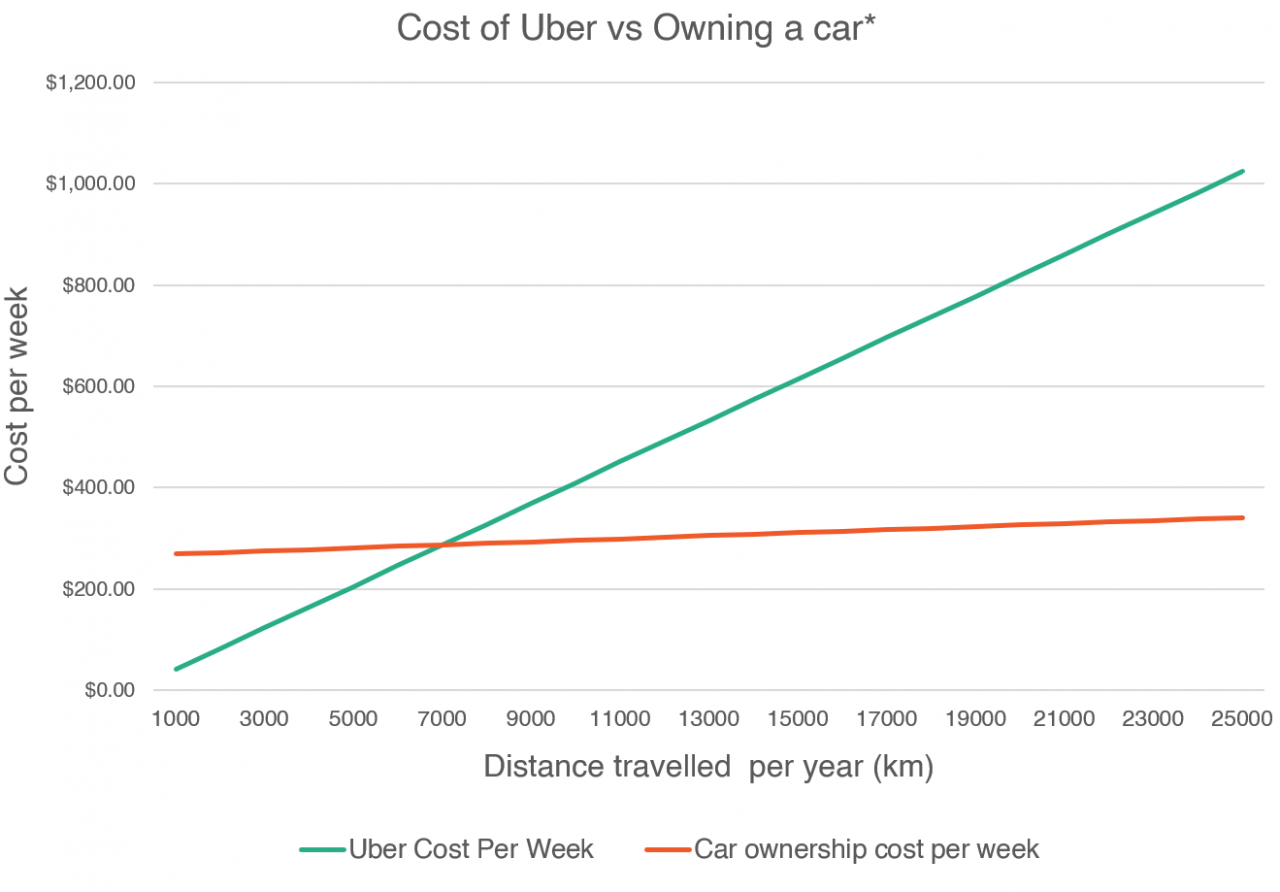

Now, by taking the cost per week of the typical household and adjusting the cost of petrol based on distance travelled per year, we can plot the cost of owning a car vs Uber on a graph.

This graph shows us that, for the typical household living in Sydney, Uber becomes more expensive than owning a car after travelling more than about 7,000 kilometres a year. This is due to the initial fixed costs of owning a car (loan repayment, registration etc).

What this graph does not show, however, is the cost for people not considered to be a typical household. The most obvious example is anyone living close to their workplace that doesn’t own a car. Unless your lifestyle fits that of this hypothetical household, it won’t be very accurate.

And even if you do fall under that umbrella, we’re making some pretty hefty assumptions – e.g. that you will always be travelling at the average speed for Sydney, and that every Uber trip is 15 kilometres in distance.

Perhaps the biggest takeaway from this graph is illustrating the fixed costs of owning a car that apply even if you only drive occasionally.

Download it for free in the App store or the Webapp below:

Important Information

The information on this website is general advice only. This means it does not take into account any person’s particular investment objectives, financial situation or investment needs. If you are an investor, you should consult your licensed adviser before acting on any information contained in this article to fully understand the benefits and risk associated with the product.

A Product Disclosure Statement for Raiz Invest and/or Raiz Invest Super are available on the Raiz Invest website and App. A person must read and consider the Product Disclosure Statement in deciding whether, or not, to acquire and continue to hold interests in the product. The risks of investing in this product are fully set out in the Product Disclosure Statement and include the risks that would ordinarily apply to investing.

The information may be based on assumptions or market conditions which change without notice. This could impact the accuracy of the information.

Under no circumstances is the information to be used by, or presented to, a person for the purposes of deciding about investing in Raiz Invest or Raiz Invest Super.

Past return performance of the Raiz products should not be relied on for making a decision to invest in a Raiz product and is not a good predictor of future performance.

Guest post written by Bondi Beauty

There are ways to still eat healthy and be fit, whilst saving money at the same time.

There’s a stigma attached to the idea that when you are fit and healthy you need to spend a lot of money to stay that way.

In-fact there are multiple ways to still save money without it effecting your healthy lifestyle.

Grab a notepad and pen and start writing out all your health-related expenses. This includes what you spend on gym memberships, fitness gear, health foods and even paid health apps you might be using; or haven’t used since you purchased.

Now, go through each item you’ve written down and see where you are spending the most money.

Do you have a monthly subscription to an app which you aren’t even using, whilst spending too much money on a gym membership that you only go to once a week?

It might be time to find a gym with no contract commitments where you don’t have to pay monthly fees, and ditch the health and fitness app if you haven’t used it for more than a few months, or ever.

There are loads of great options like Class Pass which has the option to trial for free for the first week and then select a plan for as little as $11.30 a week for six classes a month. No lock in contracts or membership joining fees and you have the flexibility to join any Class Pass registered fitness group, from Pilates, yoga to weights and even boxing.

Not only will this save you money on gym memberships, it also offer a great variety of locations, classes and is an easy way to meet new people.

What about food? Are you eating out too much?

Eating out is great, but when you calculate what you’ve spent over a week of purchasing lunch and dinner nearly every day, you’ll mostly likely find you have spent more than what a week-worth of groceries would cost.

Reduce how many times a week you eat out and reserve it for special occasions only.

There are loads of affordable ways to eat at home. Buy produce which is in season and limit the amount of meat you buy. Start experimenting in the kitchen and get cooking.

If you cook extra, you can save the leftovers and use them for lunch meals to stop you buying out every day at work. Freezer options are a great alternative to those nights when you get home too late and don’t have time to cook.

Instead of booking a table at your favourite restaurant, why not invite your friends over for a cook fest or potluck dinner. Share what yummy inspirational and healthy recipes you have found with your mates and cook up a feast. It’s cheaper and you control what you’re eating.

According to sports psychologist Dr. Jonathan Fader, when you purchase new activewear, it inspires you to work out harder. But that doesn’t mean you need a new outfit every week. Activewear can be costly.

All you need are a few key items and you can cleverly mix and match your outfits for every workout, and easily look like you have multiple outfits.

If you have excess gym accessories and activewear outfits you don’t need anymore, or have hardly used, why not sell them on eBay for some extra cash.

This is a great way to get a return on your health and fitness and have extra money on the side if you really want to treat yourself to brunch with your mates on the weekend.

Download it for free in the App store or the Webapp below:

Important Information

The information on this website is general advice only. This means it does not take into account any person’s particular investment objectives, financial situation or investment needs. If you are an investor, you should consult your licensed adviser before acting on any information contained in this article to fully understand the benefits and risk associated with the product.

A Product Disclosure Statement for Raiz Invest and/or Raiz Invest Super are available on the Raiz Invest website and App. A person must read and consider the Product Disclosure Statement in deciding whether, or not, to acquire and continue to hold interests in the product. The risks of investing in this product are fully set out in the Product Disclosure Statement and include the risks that would ordinarily apply to investing.

The information may be based on assumptions or market conditions which change without notice. This could impact the accuracy of the information.

Under no circumstances is the information to be used by, or presented to, a person for the purposes of deciding about investing in Raiz Invest or Raiz Invest Super.

Past return performance of the Raiz products should not be relied on for making a decision to invest in a Raiz product and is not a good predictor of future performance.

Even though your finances might be the last thing on your mind in your 20s, having a few financial goals will help lay the foundation for financial security in your 30s.

Of course, your goals will be different depending on your situation, however, these five can act as a place to start.

You’ve undoubtedly heard people harping on about making a budget. However, sticking to a budget doesn’t work for everyone. Even so, knowing where your money is going is incredibly important. This will help you understand where you could be spending less money and even where you could be making more money.

This could mean tracking your income and expenses in a spreadsheet or with an app, like Raiz. If you typically use a card to pay for things, these apps can sort your income and expenses into categories automatically. Ignoring your finances can land you in hot water, especially if you start accumulating credit card debt or “buy now pay later” debt such as with Afterpay.

Many people have already dipped into high-interest debt, such as having a credit card or personal loan. However, these loans don’t have to be the end of the world. Paying off your debt goes hand in hand with knowing where your money is going. It’s important that you can meet minimum repayments every month, ideally going beyond this amount. Of course, you’ll also want to avoid getting into more debt.

The thought of investing can be quite daunting, especially when you don’t know where to start. However, using a micro-investing platform such as Raiz makes it easy to invest in a diversified portfolio starting with $5. With Raiz, you don’t have to handpick stocks on your own. Plus, you can decide what level of risk you’re comfortable with. Over many years, you’ll see your money multiply with the power of compound interest and reinvested dividends. For more information on Raiz fees, click here.

If home ownership or property investment is a priority for you, now may be the time to buy, especially with the Australian market cooling. To comfortably afford repayments on a house in Australia, you’ll need to be making a significant amount. For example, in NSW, your household income would need to be $124,000 a year in order to avoid mortgage stress. You might consider setting an income goal or aim to save for a deposit in your 20s.

Even if you’re not financially independent as of yet, having an emergency fund is always an important safety net to have. Usually, a 3-month emergency fund is enough in the case that you lose your job or decide you need time off work. Once you know what your monthly expenses are, multiply that number by three and aim to have this amount saved.

Retirement should be many decades away. However, where your superannuation ends up is important now. Different super funds come with different fees and different historical returns. With compound interest, even a small difference can make you thousands more in the long-term.

After you choose a super fund that’s suitable for you, it’s important to make sure your superannuation is consolidated. Most people will have multiple jobs over their working life and sometimes this leads to having multiple super fund accounts that you’re paying fees for. Having all your money in one place will mean you’ll be making more with compound interest and only be paying one lot of fees.

For many people in their 20s, this is where you’ll enter your journey into financial independence. This means you’ll be developing habits that you’ll likely take into the rest of your life. Therefore, it’s more important than ever to make sure you’re building strong habits and goals so that you don’t end up having to reverse bad money decisions in your 30s.

Guest author: James Pointon is a Commercial Manager at OpenAgent.com.au, an online agent comparison website helping Australians to sell, buy and own property.

Download it for free in the App store or the Webapp below:

Important Information

The information on this website is general advice only. This means it does not take into account any person’s particular investment objectives, financial situation or investment needs. If you are an investor, you should consult your licensed adviser before acting on any information contained in this article to fully understand the benefits and risk associated with the product.

A Product Disclosure Statement for Raiz Invest and/or Raiz Invest Super are available on the Raiz Invest website and App. A person must read and consider the Product Disclosure Statement in deciding whether, or not, to acquire and continue to hold interests in the product. The risks of investing in this product are fully set out in the Product Disclosure Statement and include the risks that would ordinarily apply to investing.

The information may be based on assumptions or market conditions which change without notice. This could impact the accuracy of the information.

Under no circumstances is the information to be used by, or presented to, a person for the purposes of deciding about investing in Raiz Invest or Raiz Invest Super.

Past return performance of the Raiz products should not be relied on for making a decision to invest in a Raiz product and is not a good predictor of future performance.

Everyone’s spending habits differ, just like everyone’s salary differs. Learning how to spend in line with your salary whilst battling a range of competing expenses and trying not to compromise on your savings can be a difficult skill to master.

The first step to keeping your spending under control is knowing your own spending patterns. If you are a Raiz user and have linked a spending account, then you can use the My Finance feature of the Raiz app to see how much you are spending each month, and in what categories. The app will also provide you with spending alerts to your mobile phone.

You can also ask our AI powered chatbot Ashlee questions such as “how much did I spend on food last month” (to access just go into your Facebook Messenger app and search for ‘Raiz Chatbot’).

Alternatively, you can add up your expenses manually by going through and analysing your bank statement from last month (remember to include any regular debt repayments).

Once you know how much you are spending, you can then compare this amount to your after-tax income and adjust spend accordingly. Regardless if you’re spending above or below your income, we suggest a savings first mindset, that is, spend what is left after saving.

Transferring savings straight out of your pay and into an account like Raiz, where it is hard to touch the money, can be a useful strategy to regulate your spending.

The best method to calculate how much you should be spending and saving is to create a budget.

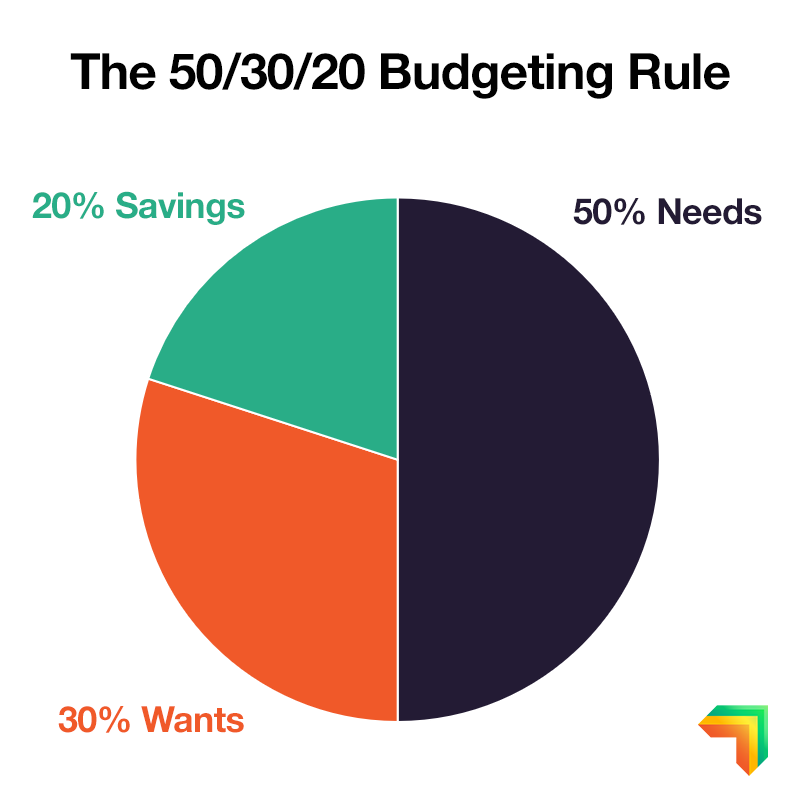

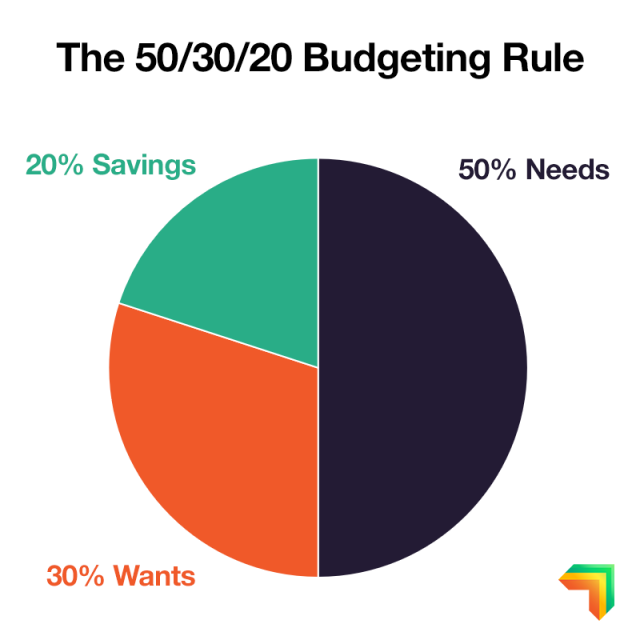

There are several types of budgeting plans out there that you can choose from. A simple budgeting strategy is the 50/30/20 budget, where you allocate 50% of income towards needs, 30% towards wants, and 20% savings. Remember the KISS principle (keep it simple stupid).

If you follow a budget like this the first thing you should do after being paid is to transfer the 20% into your special investing/savings account. We wrote about this budgeting method in our last ‘How to’ series entry, which you can read here.

You will need to continue tracking your spending to make sure you’re on course and not spending too much to force a dip into your savings. Tracking also makes it easier to adjust your budget to fit changing circumstances.

One factor that can hinder your ability to follow a budget and keep your spending in line with your salary are impulse purchases. An Impulse purchase is characterised as any purchase that is unplanned or spontaneous.

Have you ever found yourself waiting in line to pay at a supermarket, and at the last minute decide to buy a chocolate bar conveniently located next to the register? That’s a common impulse purchase, and although fairly innocuous in this example, if done repeatedly overtime, and for more expensive products, can eat into your finances.

In general, people tend to overestimate their ability to control impulsive behaviour, a phenomenon known as restraint bias. This also applies to impulse purchases. Reading this now you might be thinking it wouldn’t be that hard to resist an impulse buy, but when exposed to stimulus in a shop, be it brick and mortar or online, your self-control probably isn’t as effective as you might think.

Some strategies to help control impulse buying include:

Download it for free in the App store or the Webapp below:

Important Information

The information on this website is general advice only. This means it does not take into account any person’s particular investment objectives, financial situation or investment needs. If you are an investor, you should consult your licensed adviser before acting on any information contained in this article to fully understand the benefits and risk associated with the product.

A Product Disclosure Statement for Raiz Invest and/or Raiz Invest Super are available on the Raiz Invest website and App. A person must read and consider the Product Disclosure Statement in deciding whether, or not, to acquire and continue to hold interests in the product. The risks of investing in this product are fully set out in the Product Disclosure Statement and include the risks that would ordinarily apply to investing.

The information may be based on assumptions or market conditions which change without notice. This could impact the accuracy of the information.

Under no circumstances is the information to be used by, or presented to, a person for the purposes of deciding about investing in Raiz Invest or Raiz Invest Super.

Past return performance of the Raiz products should not be relied on for making a decision to invest in a Raiz product and is not a good predictor of future performance.

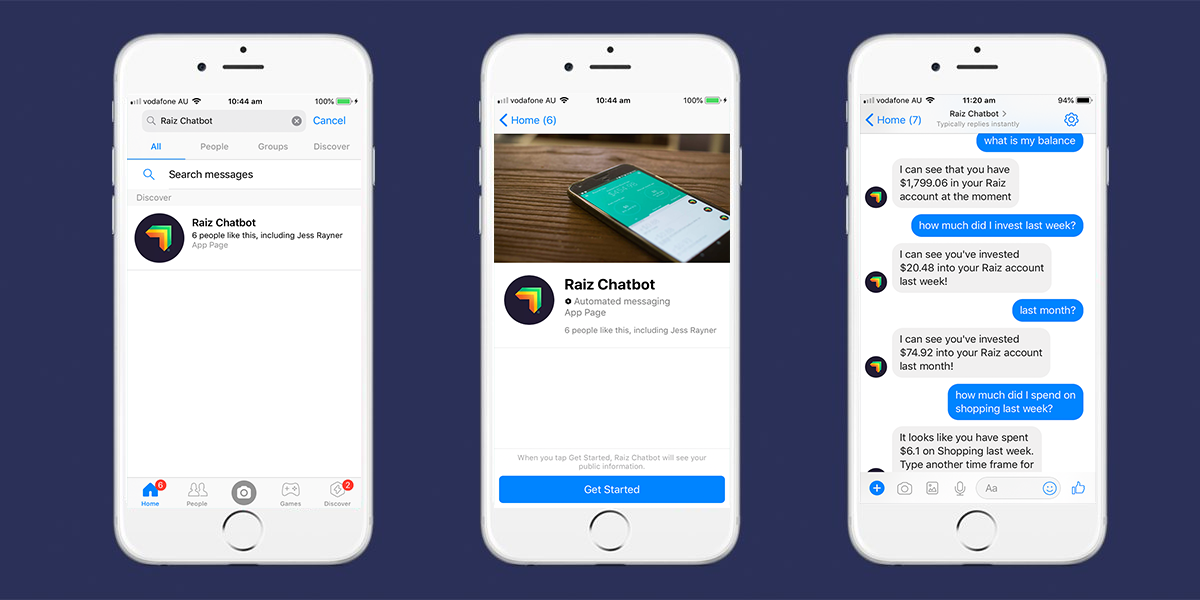

More and more Raiz users have been actively engaging with our Chatbot, Ashlee, in order to take control of and improve their financial situation. Because Ashlee is a personalised experience you can chat to her in a natural way – well nearly natural.

Ashlee – the intelligent chatbot is available through Facebook Messenger (search “Raiz Chatbot”), and can answer general questions about the market, specific questions related to your account, any support questions you have, your spending habits, and Raiz features, all without having to log into the app.

For a list of questions, check out ‘Ask Ashlee – Raiz Intelligent Chatbot Questions’.

Here are 4 smart ways that others are currently using Ashlee:

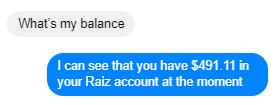

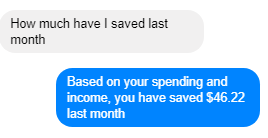

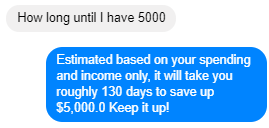

Ashlee has got you all sorted if you ever find yourself wanting to know your balance, but don’t want to login to the app. This provides an easy way to see if your investment has landed in your account, if your withdrawal has processed successfully, or to keep track of you balance.

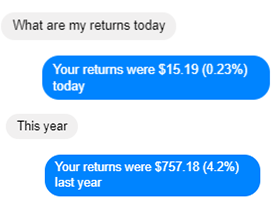

You can ask Ashlee for accounts returns for the last day, month, or year. Some users prefer this way now as they can keep track of their past performance through the message history.

Ashlee can offer tips and insights into your spending patterns based off your historic purchases and income. She can tell you how much you’re currently spending, and even project future cashflow to help you understand if you could save more or afford to eat out that night.

Some examples how users have done this include:

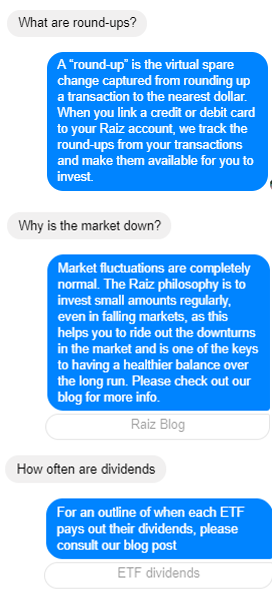

Ashlee can answer questions regarding Raiz features products and functions, making for a quick way to find answers to general customer support queries.

General customer support questions can range from learning more about specific features to word terms such as statements and dividends.

Ashlee’s purpose here isn’t to replace standard customer support channels, but rather add an extra layer on top, and allow users to quickly find answers to minor questions outside of traditional business hours.

To use, just go into your Facebook Messenger app and search for ‘Raiz Chatbot’. Please note, you will need a Facebook Messenger account to access the Chatbot.

Download it for free in the App store or the Webapp below:

Important Information

The information on this website is general advice only. This means it does not take into account any person’s particular investment objectives, financial situation or investment needs. If you are an investor, you should consult your licensed adviser before acting on any information contained in this article to fully understand the benefits and risk associated with the product.

A Product Disclosure Statement for Raiz Invest and/or Raiz Invest Super are available on the Raiz Invest website and App. A person must read and consider the Product Disclosure Statement in deciding whether, or not, to acquire and continue to hold interests in the product. The risks of investing in this product are fully set out in the Product Disclosure Statement and include the risks that would ordinarily apply to investing.

The information may be based on assumptions or market conditions which change without notice. This could impact the accuracy of the information.

Under no circumstances is the information to be used by, or presented to, a person for the purposes of deciding about investing in Raiz Invest or Raiz Invest Super.

Past return performance of the Raiz products should not be relied on for making a decision to invest in a Raiz product and is not a good predictor of future performance.

Budgeting is often pushed as an essential ingredient needed to take control of your personal finance. Whilst the concept of a budget is straight forward, it is common for people to struggle with its execution. This is especially pertinent in today’s day and age, given changing economic conditions.

One of the most popular budgeting methods often talked about is the 50/30/20 budget. This budget stipulates that you should divide your after-tax income so that:

It is important to note that these percentages are not necessarily fixed. The needs and wants percentages are the maximum amounts you should spend for those categories, leaving the 20% allocation for savings as a minimum requirement.

Over the last decade, the cost of housing/rent and utilities such as electricity have risen substantially. From September 2017 to September 2018, the Australian consumer price index (CPI), which measures the price levels of a common basket of consumer goods and services, rose by 1.9%, with the wage price index (WPI) only growing by 2.2%.

Wage growth is only just keeping ahead of increased costs of living. This is also just an average, so for some parts of the population, the cost of living would have risen faster than their wage growth.

What this means is that sticking to budgets can become harder if wants and needs begin to take up larger proportions of your income. What if your needs start to take up more than 50% of your income? If that’s the case, then you may need to scrutinise your expenses and look at where you can save money.

This could be hunting around for a cheaper phone plan or limiting usages of utilities like electricity and water to reduce bills.

If you can’t keep needs below 50%, there’s no need to panic. All budgets will be slightly different depending on the person, and the exact percentage breakdown can be altered to make it more optimised for you. Perhaps you could cut back wants to 25% and increase needs to 55%.

The bottom line is to manage your money by tracking your expenses, staying on top of and disciplined with your spending, and resolving to save/invest as much as you can afford (but remembering to leave yourself a little bit to spend on the nice things and enjoy life!).

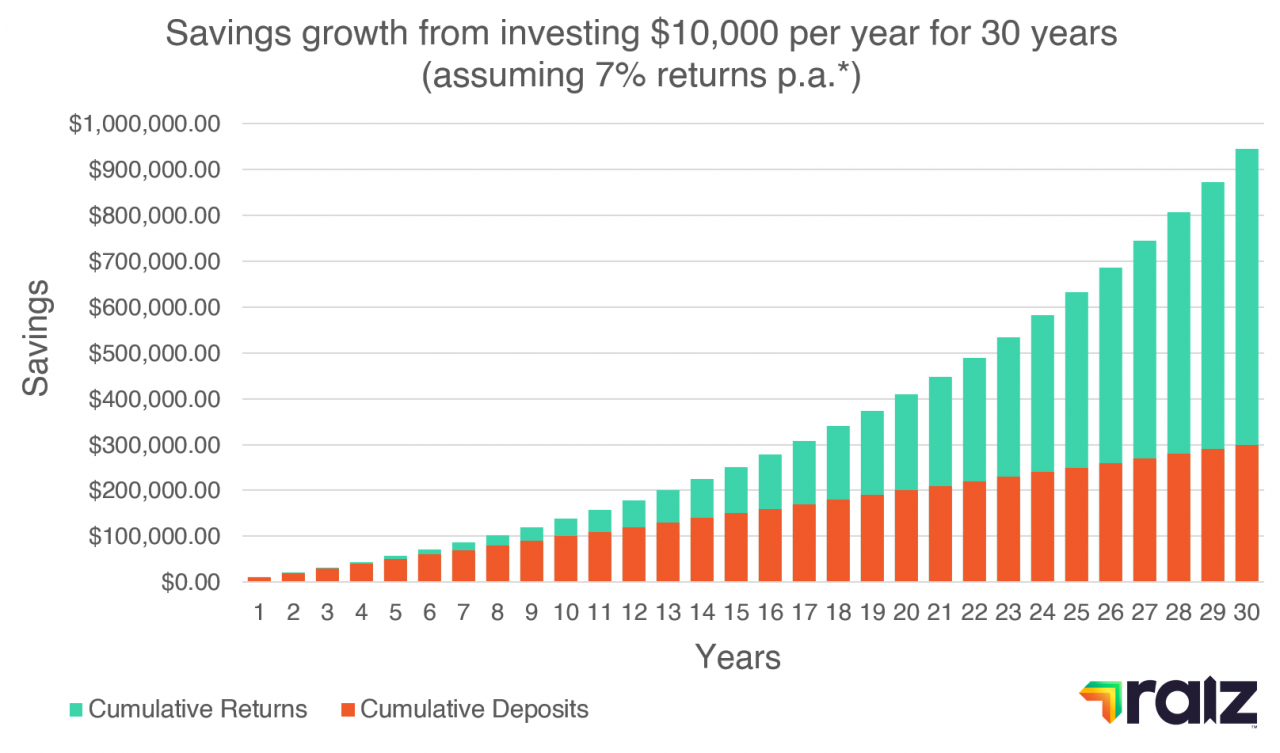

The mathematics behind compound interest shows how powerful saving and investing can be. If you were to invest $10,000 into an index fund every year, for 30 years, assuming average returns of 7% p.a. that investment will have grown to be worth $944,607. That’s a total return of $644,607.

Check out ASICS MoneySmart compound interest calculator see how much money you could have after saving different regular amounts.

Apps like Raiz can be useful tools for helping to keep track of your spending and save money at the same time. ‘My Finance’ is a free feature within the app that provides you with personalised insights and notifications on how you are spending. For more information on Raiz fees, click here.

It does this by tracking your purchases and breaking them down into categories (e.g. food and dining, bills & utilities etc.), allowing you to see how much you spend on a month to month basis.

Download it for free in the App store or the Webapp below:

Important Information

The information on this website is general advice only. This means it does not take into account any person’s particular investment objectives, financial situation or investment needs. If you are an investor, you should consult your licensed adviser before acting on any information contained in this article to fully understand the benefits and risk associated with the product.

A Product Disclosure Statement for Raiz Invest and/or Raiz Invest Super are available on the Raiz Invest website and App. A person must read and consider the Product Disclosure Statement in deciding whether, or not, to acquire and continue to hold interests in the product. The risks of investing in this product are fully set out in the Product Disclosure Statement and include the risks that would ordinarily apply to investing.

The information may be based on assumptions or market conditions which change without notice. This could impact the accuracy of the information.

Under no circumstances is the information to be used by, or presented to, a person for the purposes of deciding about investing in Raiz Invest or Raiz Invest Super.

Past return performance of the Raiz products should not be relied on for making a decision to invest in a Raiz product and is not a good predictor of future performance.