Are you eligible for Government super co-contributions?

Your super balance often forms a significant part of growing your long-term savings for retirement. It may surprise you to know there are currently government schemes available to support you in getting the most out of your super, including the co-contribution program.

You should also do your own research or discuss these potential schemes with a professional advisor to ensure that they are suitable for you.

What is the Government Super co-contribution program?

The government’s co-contribution scheme can be a great way to give your super balance a kick in the right direction. If you’re a low or middle-income earner and make personal after-tax contributions to your super fund, the government will also make a co-contribution to your super up to a maximum amount of $500 per year.

As of July 1, 2021, there are now two ways that you could be eligible for the co-contribution program:

1. Low Income Super Tax Offset (LISTO) could get you up to $500 in your super account

The Low Income Super Tax Offset (LISTO) is available to those earning $37,000 or under in the past tax year or upcoming tax years, and is designed to help offset the 15% tax applied to superannuation when it is contributed on your behalf by your employer.

If you are unfamiliar with how tax works on super contributions, rather than pay the marginal rate of tax on income going into your super fund, money that goes into your super fund is taxed at a generally lower flat rate of 15%. This is for all contributions made by either yourself or your employer.

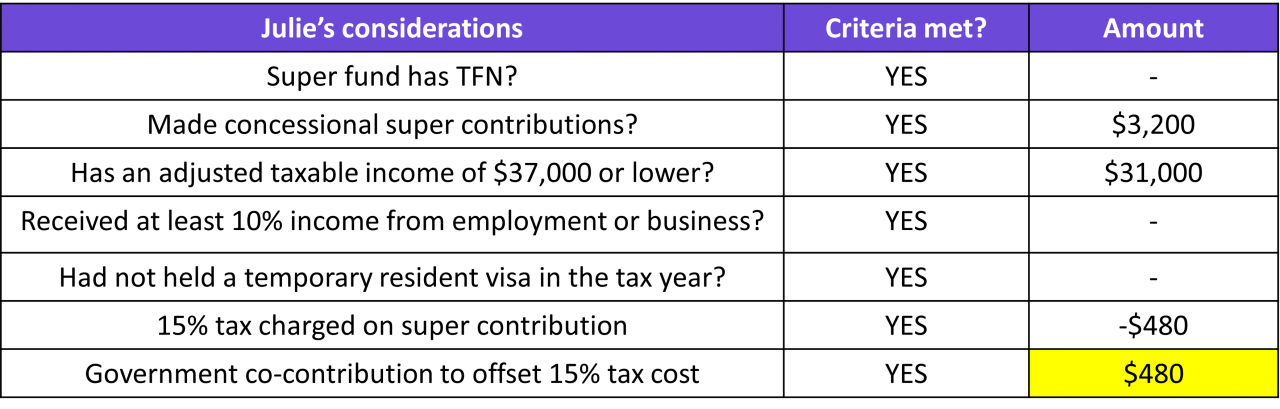

Below is an example from the ATO that explains how someone earning less than $37,000 in a year would receive a contribution from the government to offset the tax paid on their super contribution.

Julie has an adjusted taxable income of $31,000. Julie’s employers contributed $3,200 into her super fund on her behalf, meaning under the co-contribution scheme, since she has earned less than $37,000 in this financial year, the Government will reimburse $480 to offset the 15% tax paid by Julie on her $3,200 super. This will happen automatically, with no input required from Julie, because she meets the criteria.

Julie’s example, where she receives $480 as a co-contribution payment:

2. Low or middle income earners who make personal after tax contribution of $1,000 or more

A personal after-tax super contribution is a voluntary contribution you make outside of your employer doing involuntary contributions. A key benefit to this is that you may be able to claim a tax deduction on your voluntary contributions so more of your money can go towards your future than if you invested with your after-tax money. This may suit certain people due to their respective financial circumstances.

Are you eligible for the low or middle-earner co-contribution?

To be eligible for up to $500 co-contribution from the government, you must:

- Contribute $1,000 or more to their super from after-tax income

- Stay below the concessional super cap of $27,500 per year

- Meet the criteria of being a low or medium-income earner.

To see all the criteria to meet for this $500 co-contribution into your super account, click here to find more information from the ATO on if you meet the eligibility requirements.

Please remember Raiz Invest Super provides general advice only, so it is worth seeking advice from a tax adviser to see what you would need to do to be eligible.

Not eligible for these?

There are other Government schemes involving super to help you use some of your super as a deposit to purchase your first home. For more information on other these super schemes you may be eligible for, please check out our blog ‘budget initiatives helping Aussies get onto the property ladder‘.

Reductions from Raiz Invest Super fees

To give our Super fund customers the most value that we can, our administrative costs have been reduced, and we are passing these reduced costs onto our Raiz Invest Super customers.

Whether big, small or in between, reductions in fees can help your balance compound over time, meaning that your super balance could grow further on a lower cost base. To find out more about the Raiz Invest Super Fees, click here. To read the Raiz Invest Super PDS, click here.

No matter who you choose as your super fund, we hope that you get the most out of the programs available to you to help your balance grow!

Don’t have the Raiz App?

Download it for free in the App store or the Webapp below:

Important Information

If you have read all or any part of our email, website, or communication then you need to know that this is factual information and general advice only. This means it does not consider any person’s particular financial objectives, financial situation, or financial needs. If you are an investor, you should consult a licensed adviser before acting on any information to fully understand the benefits and risk associated with the product. This is your call but that is what you should do.

You may be surprised to learn that RAIZ Invest Australia Limited (ABN 26 604 402 815) (Raiz), an authorised representative AFSL 434776 prepared this information.

We are not allowed, and have not prepared this information to offer financial product advice or a recommendation in relation to any investments or securities. If we did give you personal advice, which we did not, then the use of the Raiz App would be a lot more expensive than the current pricing – sorry but true. You therefore should not rely on this information to make investment decisions, because it was not about you for once, and unfortunately, we cannot advise you on who or what you can rely on – again sorry.

A Product Disclosure Statement (PDS) for Raiz Invest and/or Raiz Invest Super is available on the Raiz Invest website and App. A person must read and consider the PDS before deciding whether, or not, to acquire and/or continue to hold interests in the financial product. We know and ASIC research shows that you probably won’t, but we want you to, and we encourage you to read the PDS so you know exactly what the product does, its risks and costs. If you don’t read the PDS, it’s a bit like flying blind. Probably not a good idea.

The risks and fees for investing are fully set out in the PDS and include the risks that would ordinarily apply to investing. You should note, as illustrated by the global financial crisis of 2008, that sometimes not even professionals in the financial services sector understand the ordinary risks of investing – because by their nature many risks are unknown – but you still need to give it a go and try to understand the risks set out in the PDS.

Any returns shown or implied are not forecasts and are not reliable guides or predictors of future performance. Those of you who cannot afford financial advice may be considering ignoring this statement, but please don’t, it is so true.

Under no circumstance is the information to be used by, or presented to, a person for the purposes of deciding about investing in Raiz Invest or Raiz Invest Super.

This information may be based on assumptions or market conditions which change without notice and have not been independently verified. Basically, this says nothing stays the same for long in financial markets (or even in life for that matter) and we are sorry. We try, but we can’t promise that the information is accurate, or stays accurate.

Any opinions or information expressed are subject to change without notice; that’s just the way we roll.

The bundll and superbundll products are provided by FlexiCards Australia Pty Ltd ABN 31 099 651 877 Australian credit licence number 247415. Bundll, snooze and superbundll are trademarks of Flexirent Capital Pty Ltd, a subsidiary of FlexiGroup Limited. Lots of names, which basically you aren’t allowed to reproduce without their permission and we need to include here.

Mastercard is a registered trademark and the circles design is a trademark of Mastercard International Incorporated.

Home loans are subject to approval from the lending institution and Raiz Home Ownership makes no warranties as to the success of an application until all relevant information has been provided.

Raiz Home Ownership Pty Ltd (ABN 14 645 876 937), an Australian Credit Representative number 528594 under Australian Credit Licence number 387025. Raiz Home Ownership Pty Ltd is 100% owned by Raiz Invest Australia Limited (ABN 26 604 402 815).