The yield curve has flipped upside down. What does this mean?

Before we dive in, let us reassure you that we will walk you through this concept step by step 😌 Don’t be scared off by jargon or big finance words.

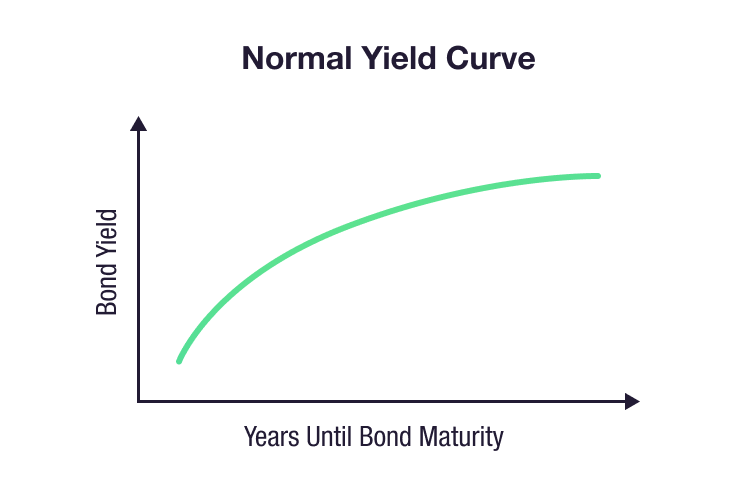

First thing’s first; let’s bring you up to speed on what a yield curve is. A yield curve indicates the expected interest rate levels in an economy over a time. A yield curve illustrates the expected interest rates at different points in time in the future, the shape the line makes is often defined as a curve.

Since the Global Financial Crisis (GFC), there have been long multi-year periods where the short-term interest rates in major economies, like the Reserve Bank of Australia (RBA) cash rate, have been at or near zero, and at higher expected interest rates in the medium and long term, e.g. 5 to 10 years. This creates an upward sloping curve.

It slopes up because interest rates rise over time, meaning the expected interest rate at year 2 is lower than year 3, which is lower than year 5.

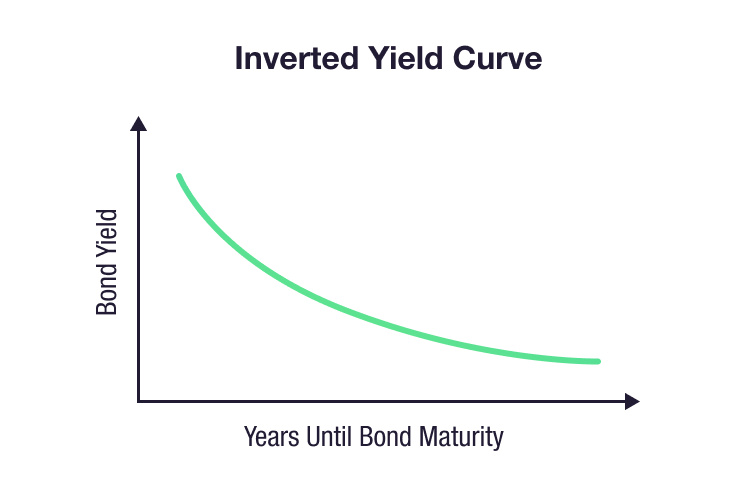

But for the first time in many years, the short-term interest rates that markets expect from Central Banks in both the US and Australia are moving higher, even higher than the medium and long-term expected interest rates.

In this case, it’s a comparison between the 2-year yield and 10-year yield, and the the 10 year yield is lower than the 2 year yield – the curve is no longer sloping up and this phenomenon is described as the yield curve “inverting” in market jargon, or turning upside down.

But what might this mean for equity markets and investing?

Do higher interest rates in the short term imply a recession is coming?

Yield curve inverting for extended periods is seen as an indication that the economy may be heading into a recession. A recession is defined as two consecutive quarters of negative growth in an economy. Higher interest rates in the short-term do not necessarily mean a recession is coming, nor that one is coming immediately. But the effect of rising short-term rates can be a move over a period from higher risk investments to lower risk cash-like products offering a higher interest rate, like an interest rate at a bank. Over time, as money movement slows in an economy, it can lead to a period of lower or negative growth.

What could higher short-term interest rates mean for markets?

While some market observers expect the inverted yield curve to be an indicator of a potential recession, the previous four times the 2-year and 10-year yield curve inverted in the US, the S&P 500 Index ended up rallying for a further 17 months, gaining 29% before peaking*. This could be because there is a period where economies adjust to higher interest rates, and that the movement of assets is gradual.

*Source: AFR Article 3rd April 2022, US wages spike triggers 10 rate rises, inverted yield curve

Equity markets and monetary policy are not the same

It’s worth noting that just as interest rates can move up and down, so can markets. It is not always clear what happens to equities as interest rates tick up, and it has been many years since this was last seen in global economies, but the data suggests that higher short-term interest rate expectations does not immediately take all of the potential upside out of the equity markets.

Don’t have the Raiz App?

Download it for free in the App store or the Webapp below:

Important Information

If you have read all or any part of our email, website, or communication then you need to know that this is factual information and general advice only. This means it does not consider any person’s particular financial objectives, financial situation, or financial needs. If you are an investor, you should consult a licensed adviser before acting on any information to fully understand the benefits and risk associated with the product. This is your call but that is what you should do.

You may be surprised to learn that RAIZ Invest Australia Limited (ABN 26 604 402 815) (Raiz), an authorised representative AFSL 434776 prepared this information.

We are not allowed, and have not prepared this information to offer financial product advice or a recommendation in relation to any investments or securities. If we did give you personal advice, which we did not, then the use of the Raiz App would be a lot more expensive than the current pricing – sorry but true. You therefore should not rely on this information to make investment decisions, because it was not about you for once, and unfortunately, we cannot advise you on who or what you can rely on – again sorry.

A Product Disclosure Statement (PDS) for Raiz Invest and/or Raiz Invest Super is available on the Raiz Invest website and App. A person must read and consider the PDS before deciding whether, or not, to acquire and/or continue to hold interests in the financial product. We know and ASIC research shows that you probably won’t, but we want you to, and we encourage you to read the PDS so you know exactly what the product does, its risks and costs. If you don’t read the PDS, it’s a bit like flying blind. Probably not a good idea.

The risks and fees for investing are fully set out in the PDS and include the risks that would ordinarily apply to investing. You should note, as illustrated by the global financial crisis of 2008, that sometimes not even professionals in the financial services sector understand the ordinary risks of investing – because by their nature many risks are unknown – but you still need to give it a go and try to understand the risks set out in the PDS.

Any returns shown or implied are not forecasts and are not reliable guides or predictors of future performance. Those of you who cannot afford financial advice may be considering ignoring this statement, but please don’t, it is so true.

Under no circumstance is the information to be used by, or presented to, a person for the purposes of deciding about investing in Raiz Invest or Raiz Invest Super.

This information may be based on assumptions or market conditions which change without notice and have not been independently verified. Basically, this says nothing stays the same for long in financial markets (or even in life for that matter) and we are sorry. We try, but we can’t promise that the information is accurate, or stays accurate.

Any opinions or information expressed are subject to change without notice; that’s just the way we roll.

The bundll and superbundll products are provided by FlexiCards Australia Pty Ltd ABN 31 099 651 877 Australian credit licence number 247415. Bundll, snooze and superbundll are trademarks of Flexirent Capital Pty Ltd, a subsidiary of FlexiGroup Limited. Lots of names, which basically you aren’t allowed to reproduce without their permission and we need to include here.

Mastercard is a registered trademark and the circles design is a trademark of Mastercard International Incorporated.

Home loans are subject to approval from the lending institution and Raiz Home Ownership makes no warranties as to the success of an application until all relevant information has been provided.

Raiz Home Ownership Pty Ltd (ABN 14 645 876 937), an Australian Credit Representative number 528594 under Australian Credit Licence number 387025. Raiz Home Ownership Pty Ltd is 100% owned by Raiz Invest Australia Limited (ABN 26 604 402 815).