How to: Invest in your kid’s future

Kids can be impulsive, cry when they don’t get what they want, or be ecstatic seeing Santa’s presents under the tree. Parents have to convince a toddler why they aren’t allowed to get into the washing machine with their clothes, all the while thinking what’s to come next.

After investing so much time into your kid’s development, a sought-after milestone is to see them start their adult lives with sound financial literacy, coupled with some of their own money set aside – valuable tools that can help them lead happy and successful lives.

Research published in 2018 by the Australian government found that the minimum cost of raising one child, for a low-income family, ranges from $140-170 per week, or $7280-8840 per year – and that’s the bare minimum. Moreover, a survey conducted by the ABC in 2018 found that over half of Aussies aged 18-29 have less than $5k in savings, whilst over a quarter have more than $5k in debt (excluding HELP/HECS debt).

Whilst money won’t be the sole factor that affects your kid’s future, equipping them with financial life skills and a little bit of extra cash can go a long way in adding a boost later in life.

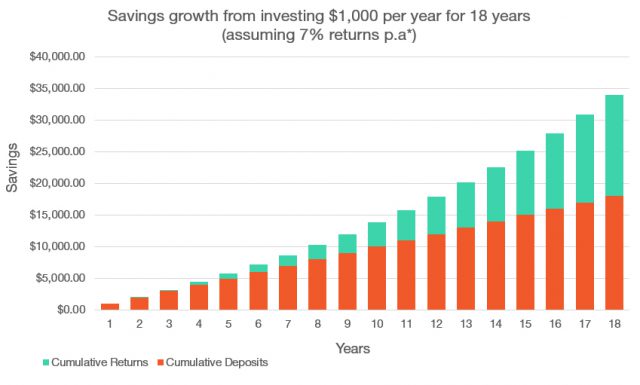

The earlier you start, the more time money has to grow and take advantage of compound returns. For example, with the power of compounding, if you were to invest $1,000 every year for 18 years, assuming average returns of 7% p.a.*, that investment could grow to be worth $34,000, off your $18,000 investment. That’s a total return of $16,000.**

How’s that for an 18th Birthday present?

Where can I invest in my kid’s future?

If you’re putting money aside for your kids, and want to see those savings grow over time, there are multiple places to consider investing your money.

Savings Account

Savings accounts won’t earn you a lot of interest, with their primary benefit coming in the form of virtually no risk (the Australian Government guarantees deposits up to $250k in Authorised Deposit-taking Institutions). Our research found that 85% of Australians don’t know the interest rate on their average savings account, so be sure to be vigilant when comparing rates, as some accounts offer higher introductory rates before being reduced significantly.

George Lucas, our CEO says: “Many Australians are completely unaware of the best options to protect and grow their income and think they’re getting 2-3 per cent on their savings accounts when, depending on the bank, it’s often less than 1 per cent.”

“This is due to the way saving accounts are advertised with introductory offers. At this interest rate, if Australians are using their savings accounts to save money, with inflation, the opposite is happening and they’re actually going backwards.”

This is an important consideration when saving for kids, as your kids will be likely living at a time with higher cost in living in the future e.g. housing & petrol, so the money you save for them might not be worth as much as it is today if you keep it only in a savings account.

Other features to consider are minimum and maximum account balances, account-keeping fees if any, the conditions needed for any bonus interest, and whether a linked account is required.

Investment bond

Investment bonds are like managed funds, combined with an insurance policy. Your money is pooled with money from other investors, with an investment manager making the day to day investment decisions. The main advantage of an investment bond is that they can be a tax effective way to invest for the long-term, provided certain conditions are met.

The potential tax benefits and long-term nature of investment bonds means they can make for a nice way to invest for your kid’s future as they can benefit from potentially a lower tax rate on earnings received after 10 years.

Raiz Kids

Raiz Kids is a simple way to save and invest for your children and/or dependents who are under the age of 18. It essentially works the same as your normal Raiz account, which lets you invest small amounts regularly into one of six diversified portfolios that are invested across cash, bonds, domestic and international shares.

By adding a partition to your Raiz account, it allows you to nominate a portion of your Raiz balance (or even all of it) to be transferred to your kid’s when they turn 18. Nothing is set in stone, and you can adjust the Raiz Kids portion at any time. Once your children reach the age of 18, they are then able to open their own Raiz Account, with the option of having these funds transferred into their account.

Since inception, the avg. Raiz investor has made 12.4% p.a.* as of Dec 2018 (return includes all fees but before the $3.50 monthly maintenance fee). For more information on Raiz fees, click here.

Teach along the way

It’s also important that setting aside money for your kid’s future is tied together with teachings in financial literacy. It would be a wasted opportunity to be setting them up with additional cash if they don’t know how to responsibly manage it. Basic financial literacy is an important skill set that your kids will take with them throughout their entire lives.

Pocket money is one of the most popular ways to teach kids the value of money at a young age. Paying them in cash for completing helpful chores and jobs gives them a tangible experience with money, allowing them to see their piggy bank grow before their eyes.

As they get older, help them open a savings account, and encourage them to set savings goals. Involve them in writing out shopping lists before visits to the supermarket by explaining what you need, the price of those things, and how much money you have to spend. Consider setting up a Raiz kids account, which can give them basic exposure to the market and compound interest.

As they make their way through their teenage years, be sure to keep on building on what you have taught them.

*Past performance is not an indication and should not be relied on for future performance.

**Return estimated for the sake of simplicity as past performance is no indication of future performance – see ASICS managed funds fee calculator to get an estimate on how fees and costs can affect your investment. Return estimate is net of MER. The value is a future value, not a present value.

Don’t have the Raiz App?

Download it for free in the App store or the Webapp below:

Important Information

The information on this website is general advice only. This means it does not take into account any person’s particular investment objectives, financial situation or investment needs. If you are an investor, you should consult your licensed adviser before acting on any information contained in this article to fully understand the benefits and risk associated with the product.

A Product Disclosure Statement for Raiz Invest and/or Raiz Invest Super are available on the Raiz Invest website and App. A person must read and consider the Product Disclosure Statement in deciding whether, or not, to acquire and continue to hold interests in the product. The risks of investing in this product are fully set out in the Product Disclosure Statement and include the risks that would ordinarily apply to investing.

The information may be based on assumptions or market conditions which change without notice. This could impact the accuracy of the information.

Under no circumstances is the information to be used by, or presented to, a person for the purposes of deciding about investing in Raiz Invest or Raiz Invest Super.

Past return performance of the Raiz products should not be relied on for making a decision to invest in a Raiz product and is not a good predictor of future performance.