5 things to consider when buying a home

By Rachel Gopez – uno Home Loans

1. Where do I start?

Buying a property can be one of the most stressful times in your life. A lot of research, time and effort is required to find the ideal house. There are many things to consider, so it helps to have a structured set of steps to follow when starting the process.

A great starting point is to work out a budget based on your deposit and how much you can borrow. It can be tricky to pull numbers out of thin air, so using an online calculator such as uno’s borrowing calculator is a great tool to help you work this out. Once you get your pre-approval secured, you’ll have a good estimation of what purchase price you’re looking at. After finalising your exact budget, you can get started on the fun part: finding your dream home!

2. How much money do I need for a deposit?

A deposit isn’t the exact same amount for everyone. When calculating your home deposit, most lenders generally require 10% of the property’s value and sometimes only 5%. For example, if the property you want to buy is valued at $800,000, the deposit required would usually be between $40,000 (5% of $800,000) and $80,000 (for a 10% deposit).

With a 5% deposit, it needs to comprise genuine savings. This doesn’t include money from a parent or third party (this is known as a gift) and must be savings in a bank account.

The more money you have saved for a deposit, the better. “Having at least a 20% deposit is your best option, as it saves you from paying lenders mortgage insurance,” says uno Home Loans team leader, Chris McNaughton.

3. Can I buy a property with no deposit saved?

So you’re not a famous blogger and have no money saved yet? All is not lost! A guarantor loan is one way to buy property when you don’t have a deposit. A guarantor is legally responsible for paying back the entire loan if you cannot make the loan repayments. The guarantor is usually a family member and will also have to pay any fees, charges and interest. Learn more about guarantor loans here.

4. What costs are involved in buying a home?

The exact costs involved in buying property depend on which state you live in. This is due to the variance in house prices, stamp duty and legal costs. You can calculate how much stamp duty you’ll have to pay, based on your state, here. You’ll also have to pay a transfer fee and a mortgage registration fee. The transfer fee is roughly around $200-$300 and the mortgage registration fee is around $100-$150.

The legal work involved in preparing the contract of sale and thoroughly reading all legal documents is called conveyancing. A conveyancer can help you arrange and make changes to a contract. The price range for this service is typically around $600 to $1,500.

5. How much does an average house cost in Australia?

Australian property prices are talked about more than Australia’s Prime Minister (who is it again?). Asking the cost of a house in Australia is like asking how much a latte costs: it really depends on where you are. Median property prices in each state change month-to-month, but you can find updated data from property analytics company CoreLogic.

Remember, buying a home is one of the biggest decisions you’re likely to make in your lifetime. You want to do your research and take it seriously.

About Author

Rachel Gopez is Content Producer at uno Home Loans, the online mortgage broker.

Looking for a new home loan? What used to take days with banks and brokers can how be done in less than 10 minutes – from your lap top or mobile phone. uno is an online mortgage broker with one mission: to help you win at home loans. Whether you’re a home buyer or looking to refinance an existing loan, uno puts the power back in your hands. Visit www.unohomeloans.com.au

It’s important to note that the information we give here is general in nature – no matter how helpful or relatable you find our articles. Even if it seems like we’re writing about you, it’s not personal or financial advice. That’s why you should always ask a professional before making any life-changing decisions.

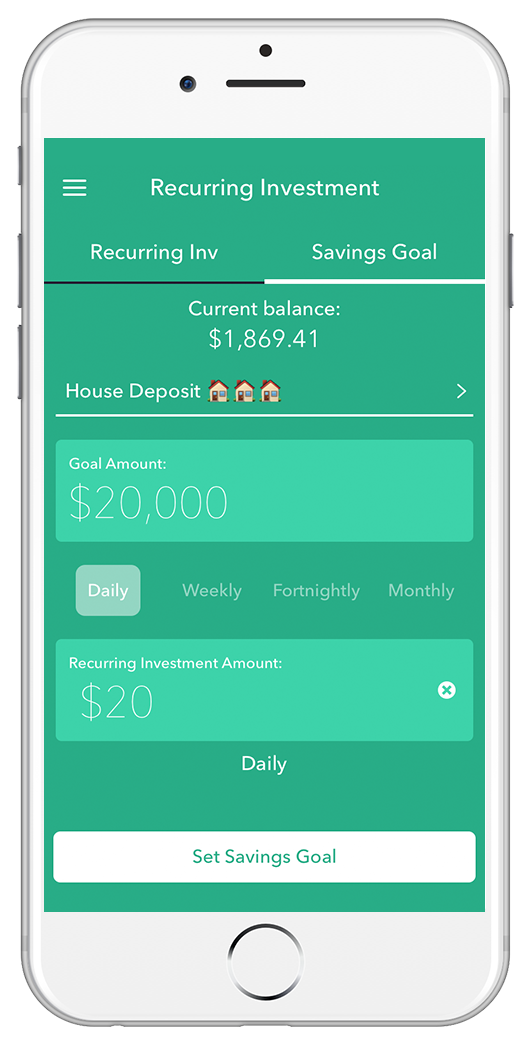

Raiz: Need a way to start saving for a house deposit?

Use Raiz to set up a Savings Goal to help you reach that house deposit easier. While just having round-ups turned on might take longer than you’d like to save this up, you can also set up a recurring investment or invest lumpsum deposits whenever you have free cash to spare. You can also manage your budget through the MyFinance feature, which shows an overview of your current and future cashflow. By automating your Savings plan, you can spend more time on looking for your perfect home!

Don’t have the Raiz App?

Download it for free in the App store or the Webapp below:

Important Information

The information on this website is general advice only. This means it does not take into account any person’s particular investment objectives, financial situation or investment needs. If you are an investor, you should consult your licensed adviser before acting on any information contained in this article to fully understand the benefits and risk associated with the product.

A Product Disclosure Statement for Raiz Invest and/or Raiz Invest Super are available on the Raiz Invest website and App. A person must read and consider the Product Disclosure Statement in deciding whether, or not, to acquire and continue to hold interests in the product. The risks of investing in this product are fully set out in the Product Disclosure Statement and include the risks that would ordinarily apply to investing.

The information may be based on assumptions or market conditions which change without notice. This could impact the accuracy of the information.

Under no circumstances is the information to be used by, or presented to, a person for the purposes of deciding about investing in Raiz Invest or Raiz Invest Super.

Past return performance of the Raiz products should not be relied on for making a decision to invest in a Raiz product and is not a good predictor of future performance.