Investing is a marathon, not a sprint

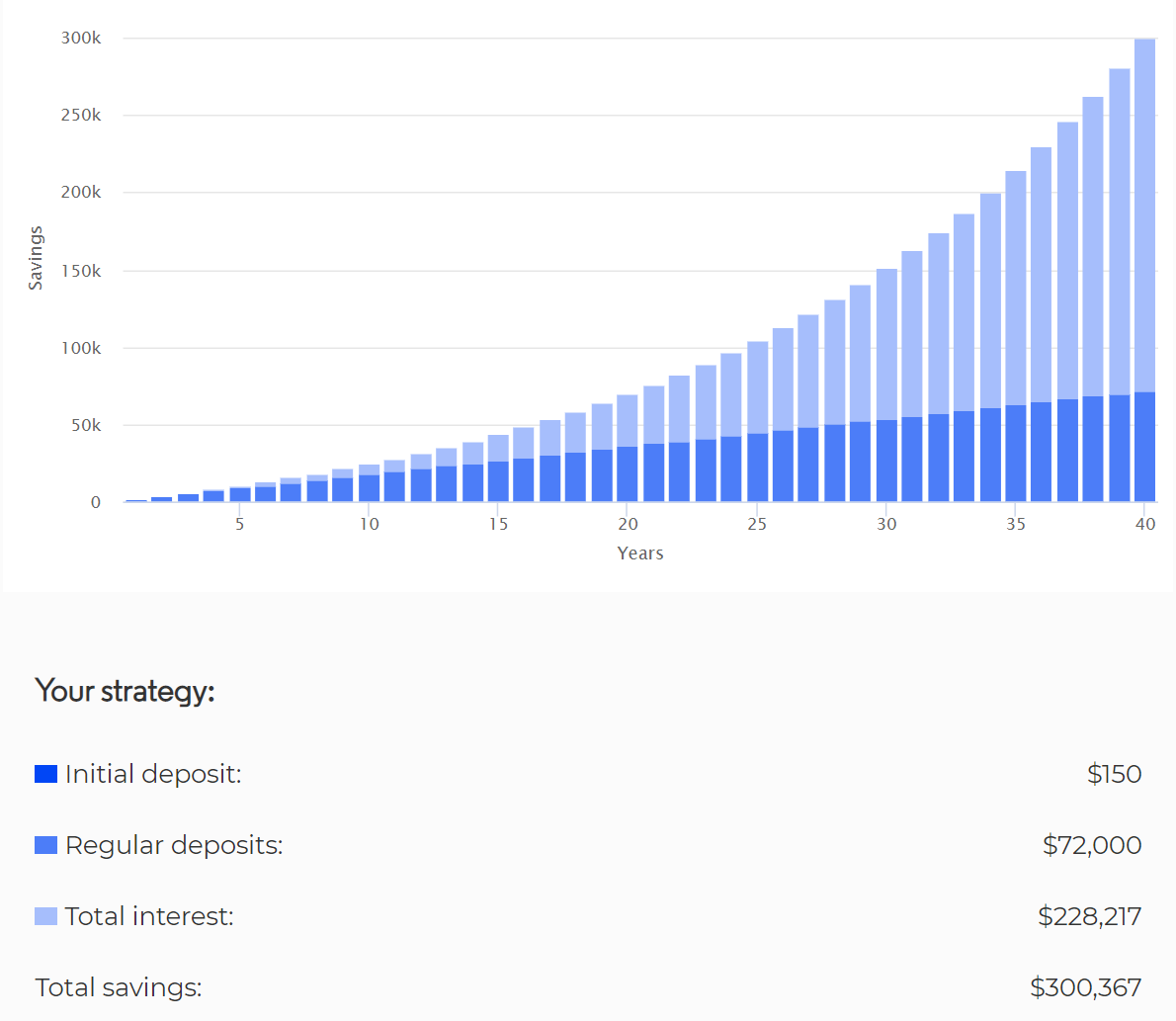

Any marathon runner will tell you: You don’t think about all 42 kilometres at once. That would be too overwhelming. Instead, picture the race in chunks: 5km, 10km, or even one kilometre at a time. Manageable chunks. This same philosophy can be useful when saving for your post-work life, especially when it’s still decades away. While the idea of saving a big enough chunk of money to retire comfortably may feel like a near-impossible feat, investing just $150 or so per month in your 20s or 30s seems much more reasonable — and that still may get you to your desired savings goal by retirement age, provided you’re disciplined, start early, and hit your “splits,” as runners would say. For the sake of simplicity, let’s set aside inflation, fees, taxes and dividends. Yes, those things are important, but it’s more important that you just get started, save regularly, and experience the power of compounding returns. Here’s what this example could look like, assuming market returns of 6% p.a.*:

source: moneysmart.gov.auOkay, deep breaths. We’re going to walk you through these targets, and explain why they’re more reachable than you might think — and why, if you’ve hit 30 and haven’t saved that much, it’s not too late. The first thing you’ll probably notice about this chart is that the growth in your money exponentially increases as time goes on. This is due to the power of compounding returns. You’ve probably heard about compounding before, and not for lack of good reason, since understanding this concept can be super valuable for your finances. It’s often described as interest on interest, which means that if your money grows by 6% in a year, and you don’t withdraw any of that money, the next 6% you earn will be a larger dollar increase, since it is growing from a larger base than the first year. This goes on and on, giving your money the potential to grow at an exponential rate, which explains the growth in our chart above. The human brain is notoriously bad at estimating exponential growth, so a useful rule of thumb you can use is the rule of 72. This is a rough calculation of how many years it takes to double an investment and is calculated by dividing your rate of return (interest rate) by 72. If you earn a consistent 6% p.a. on your money, for example, it will take roughly 12 years to double your money. With a disciplined and regular saving/investing strategy, it is entirely possible to start a humble retirement account in your 20s and 30s and still be on target to retire with a decent nest egg. You just have to hit your splits. It is important to keep in mind that although 6% p.a. is a reasonable estimate for stock market returns over the long term, it is by no means a guarantee. All investments carry risk, and it’s impossible to know the actual return you will make on your investments in the future. Another thing to keep in mind about your contributions: As you get older, you’re likely to increase your income, so it wouldn’t be unrealistic to increase your monthly $150 to something more substantial, adding more fuel to your marathon and potentially boosting your final retirement fund. You can think about saving for retirement just like you would if training for a marathon. Instead of just waking up one day and trying to sprint 42km, you need to train, and start working on your financial fitness. With our Round-Ups and automatic investing features, you can hit your splits whilst living your everyday life. For more information on Raiz fees, click here. There’s no denying the power of regular savings, time and compounding. A journey of a marathon begins with the first step. A journey to $1 million begins with your first $100 investment. *Return estimated for the sake of simplicity as past performance is no indication of future performance – see ASICS managed funds fee calculator to get an estimate on how fees and costs can affect your investment. Return estimate is net of MER. The value is a future value, not a present value.